Dodd Kittsley, CFA & Davis Director of ETFs, discusses investment themes, types of companies, and the attractive growth / low multiple companies populating the portfolio

Transcript

Dodd Kittsley:

We've seen significant interest in DUSA and I think the reason for it is it's very well set up for the environment we're in and addresses a lot of the concerns on the minds of investors today whether that's an pending recession. The impact of higher interest rates we've gotten so used to rates being so low for so long, uh, that it has been unclear for a lot of folks how higher rates are going to impact.

For example companies debt position. and things of that nature, so DUSA is very well set up to address the concerns again, forefront on people's minds.

If you take kind of a top-down view, which a lot of investors like to take, it is a portfolio that has several wonderful attributes. The first is that it has a historical earnings growth rate that is higher than the overall market. Yet at the same time, the portfolio and average is trading at a discount that is nearly 40% less than the market.

So, you're getting great value for businesses that are actually growing earnings at a rate that's not only level with the market, but slightly better at the current state.

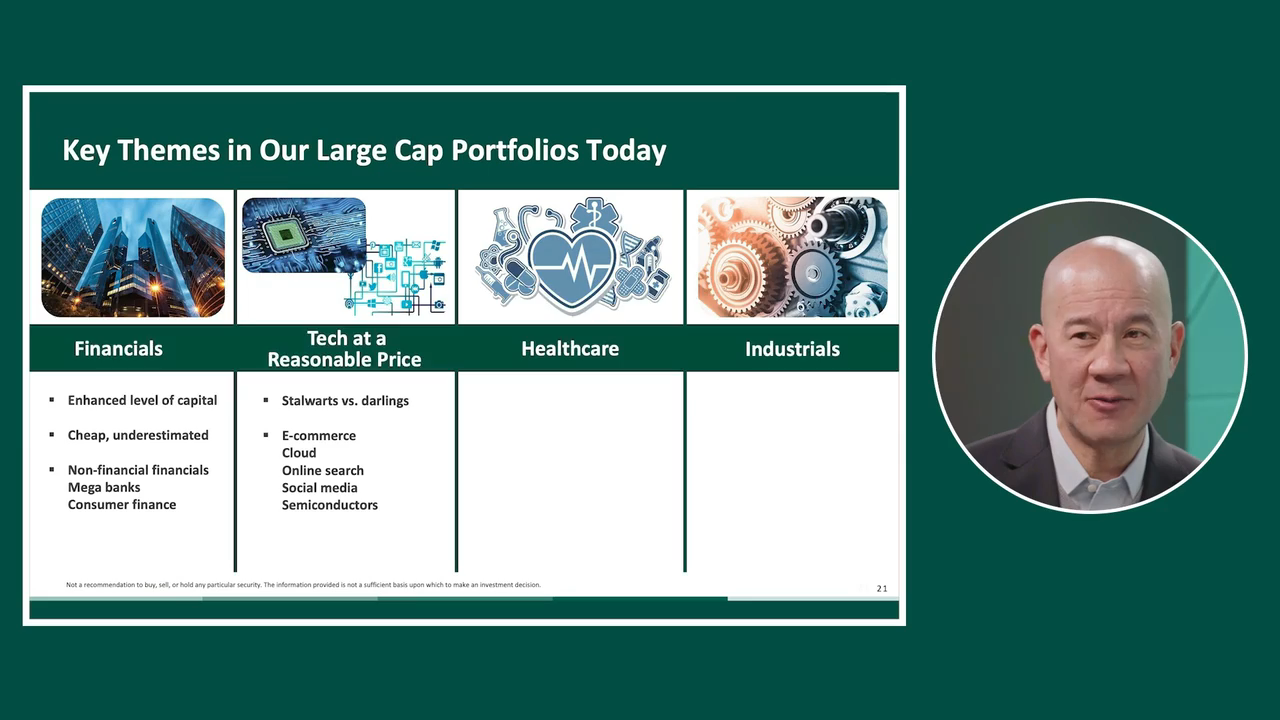

But the real ingredient to our secret sauce is selectivity. It's what goes into the 27 names currently in DUSA today, and we've got an incredibly high bar. Again, what you don't own is as important as what you do own in a market that we're expecting in the environment, we're expecting going forward.

DUSA is a very uniquely positioned and, you know, we are benchmark agnostic, so it truly is research-based bottom-up. there's not an intention to have exposure to a particular theme or a particular market segment or sector.

That's kind of spurious based on, again, the best ideas that our research team has. That being said, there are some commonalities and themes that we think give tailwinds where we want to be participating in that industry, but we also want the best of the best in there.

So the first, I would say, is an overarching category is we're looking at growth companies that are potentially undervalued, or it's underestimating the true earnings growth that these companies can achieve. They're competitive moats, they're scale in the industry. So that would include a lot of areas of technology. Some cloud computing companies, some consumer, online consumer companies, those sort of areas, where many folks will say, look, I thought you were a large cap value.

What do you have? Companies like Meta or companies like Alphabet in your portfolio or Microsoft? Those are tech companies. It's like, yeah, we see tremendous value. Our research team sees tremendous value in there based on the trajectory of what those companies can accomplish and their spots in the marketplace.

If you transition to value, we're actually looking at value very different than an index does, values such a diverse segment of the market to begin with, but we're essentially looking for growth companies in disguise. We're looking for, you know, where people are underestimating the growth of value companies. And financials is a great example there.

Financials are very hard to track on earnings. Earnings can be this kind of nonlinear path, especially with accounting for loss provisions and what have you. So we think the market kind of overreacts sometimes and penalizes the volatility of earnings in financials yet the long-term trajectory and we are long-term investors and our shareholders are as well. We think we can take advantage of that through time arbitrage in identifying mispricing in some value segments. Healthcare's another really emerging theme in the portfolio, maybe wasn't so a couple of years ago, but we're seeing great opportunity there.

In areas where most people wouldn't probably suspect when you think healthcare, we're not in the big pharma, but where we are very interested in is in companies that are adding value to the system, adding value to an inefficient system that is felt by the end consumer in felt overall by the whole medical

community at large. So a good example that would be Viatris, which is a real dominant global, yes pharmaceutical, but they play in the generics and have a lot of off patent brands.

And we've seen a major demographic shift where the vast majority of medications these days are now generic and not those brand names that people have to pay up for in a big way.

We also are invested in diversified healthcare companies that are adding value to the system through their investments in technology and integration and making things much more connected in an industry where I think most of us have probably had pretty bad experiences over time.

So the coordination with companies like Humana and Cigna have massive, massive opportunities as well as their role in Medicare Advantage, which we know has had some short-term bumps along the road, but long-term is going be a place where it's critical for our nation, and it's critical for our population

to have very good and more efficient healthcare than we have today.

More Videos

AI: Separating Hype from Opportunity (4:17)

Incorporating DUSA in a Portfolio Allocation (1:44)